Depletion: Definition & Overview

There can be hundreds of different terms and phrases to understand when it comes to accounting. Each one plays a little bit of a different role compared to the others. Yet, many of them work harmoniously together. Depletion rate, for example, plays an integral role when extracting natural resources.

It can be incredibly important for some types of companies, but there can be a lot to know. That’s why we created this guide to break down how depletion works. Keep reading to learn more, including how it works, some different methods, and how to calculate it.

![]() Table of Contents

Table of Contents

KEY TAKEAWAYS

- Depletion is similar to amortization and depreciation, but it’s used for companies that sell natural resources.

- There are two methods of calculating depletion: percentage depletion and cost depletion.

- Several types of costs impact depletion at different parts of the production cycle. They include acquisition costs, exploration costs, development costs, and restoration costs.

What Is Depletion?

Depletion in accounting is the process of allocating the cost of recoverable units of a natural resource. This expense is in a systematic and rational manner as those units are extracted or consumed.

The depletion rate is the percentage by which the recoverable units are divided into expenses for a given period. The accounting method used must apply, and must allocate costs in a manner that reflects the physical realities of extracting or consuming the resource. The depletion rate must be consistently applied to follow generally accepted accounting principles.

The depletion rate can increase or decrease, but it depends on how management intends to recover the natural resource costs associated. A higher depletion rate means recoverable costs are recognized as expenses at a faster rate. This is often used when management wants to recover the costs associated with a natural resource as quickly as possible.

A lower depletion rate means that recoverable costs are recognized as expenses at a slower rate. This is often used when management wants to recover the costs associated with a natural resource over a long-range period.

When estimating recoverable units, management must use a reasonable and consistent method. There are two methods of calculating depletion: units-of-production method and straight-line method.

The first method allocates costs based on the number of recoverable units extracted or consumed.This method is often used when the recoverable units can be easily measured, such as in the case of minerals or oil.

The second allocates costs evenly over time, regardless of the recoverable units extracted or consumed. This method is often used when the recoverable units cannot be easily measured, such as in the case of timber.

The concept of depletion is similar to the concepts of amortization and depreciation. For example, it distributes the reduction in resources across extended periods. Rather than recording the full amount of depletion costs as expenses, it is capitalized. When the resources are extracted, the full depletion costs are then recognized as depletion expenses either by units or evenly over time.

Moreover, you can measure depletion over a long- and short-range period. You can use the clinical evidence provided on a timely basis to make adjustments, but it’s important to consider economic conditions at the time.

How Depletion Works

Turning raw materials into a product comes at a cost. Oil, for example, goes through the following process:

- Drilling

- Fracking

- Refining

- Production

This process takes place before it’s put up for sale as a product. The catch is that it’s a natural resource with a finite accessible amount. The extraction costs increase is always accompanied by the natural resource amount decrease.

Depletion works a lot like depreciation and amortization. Depletion helps find the natural resources, which is the company’s assets and get recorded on the company’s balance sheet.

When resources get extracted, the capitalized expenses get recognized across the fiscal periods.

The depletion of energy is something the natural resource industry must account for.

Let’s discuss how to determine the natural resource extraction expenses. You have to consider the costs in each phase of production and which costs can be counted as extraction expenses.

The following costs impact depletion:

Acquisition: Costs associated with purchasing an asset or earning a new client. Many times this includes the land rights for a property that contains natural resources.

Exploration: These expenses come with surveying and searching the land to find the natural resource.

Development: The cost of preparing the land for drilling, construction, mining, etc.

Restoration: The extraction process is now complete. As such, there are expenses associated with restoring the land to its original state.

Depletion Methods

There are two main methods of calculating depletion– percentage depletion and cost depletion. One is more heavily used than the other, and the IRS has certain requirements on which method to use with specific natural resources.

Percentage Depletion

This allocates expenses by assigning a fixed percentage value to gross revenue from the property during the tax year. The fixed percentage gets multiplied by the gross income to find the total capitalized costs depleted.

Suppose $100 million worth of minerals gets extracted. The fixed percentage is 20%. Therefore, there would be $20 million in capitalized costs depleted to complete the extraction. The fixed percentage rate is based on factors that impact that specific natural resource industry.

The percentage depletion method depends on estimations of factors that impact the percentage. So this method isn’t always trusted or accepted.

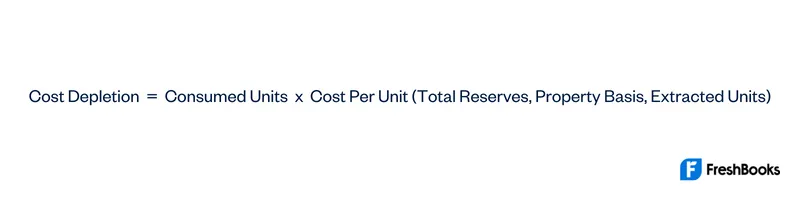

Cost Depletion

Cost depletion is more widely accepted since it’s easier to calculate and works less with estimations. This depletion method spreads out the natural resource’s depletion across the full lifespan of the resource.

How Do You Calculate Depletion?

Example of Depletion

To better understand how to calculate it, let’s plug in an example. Let’s say that Company X owns a $500,000 quartz mine and made an initial investment of $60,000 for the property and development.

Over the life of the mining project, they estimate that they can gather 5,500 pounds of quartz. Within the first year, the project harvests 600 pounds of quartz.

To translate that to a formula would look like this:

60,000 600 5500= $6,545.45 cost depletion

So the depletion expense for the first year would be $6,545.45. This information would get included on Company X’s balance sheet and their income statement for the year.

Summary

Overall, depletion is a useful calculation in accounting for a business that sells natural resources. The two different methods let companies estimate or get exact figures on depletion costs in extraction.

It also allows for the costs to become capitalized over extended time periods. The cost depletion method is usually more trusted than others.

FAQs about Depletion

Depletion is not the same as depreciation, although they do have some similarities.

Only natural resources can deplete since there’s a limited amount of each type available. As a company uses the resource, they’re also depleting the availability of the asset along with the number of future sales.

It depends on the type of resources you want to claim. You need to use appropriate methods for resources like mines, gas wells, etc.

The depletion allowance is a tax deduction. Energy companies that sell natural resources can claim to account for the gradual depletion of energy.

Share: